Maximizing Home Equity: Seizing a Once-in-a-Lifetime Financial Opportunity

Home Equity Loan vs. HELOC: Making the Right Choice for Your Financial Needs

Understanding Home Equity: The Foundation of Your Borrowing Power

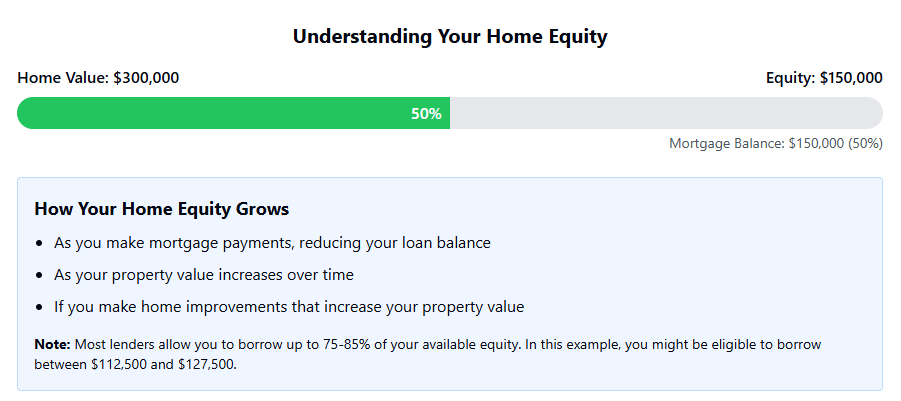

Before diving into the specifics of home equity loans and HELOCs, it's important to understand what home equity actually is. Simply put, home equity is the portion of your home that you truly own—the difference between your home's current market value and what you still owe on your mortgage and other liens.

For example, if your home is worth $300,000 and you have $150,000 left on your mortgage, you have $150,000 in equity. This equity grows in two ways: as you pay down your mortgage and as your property value increases over time.

This equity isn't just a number on paper—it's a valuable financial resource you can tap into when needed, typically through a home equity loan or a HELOC.

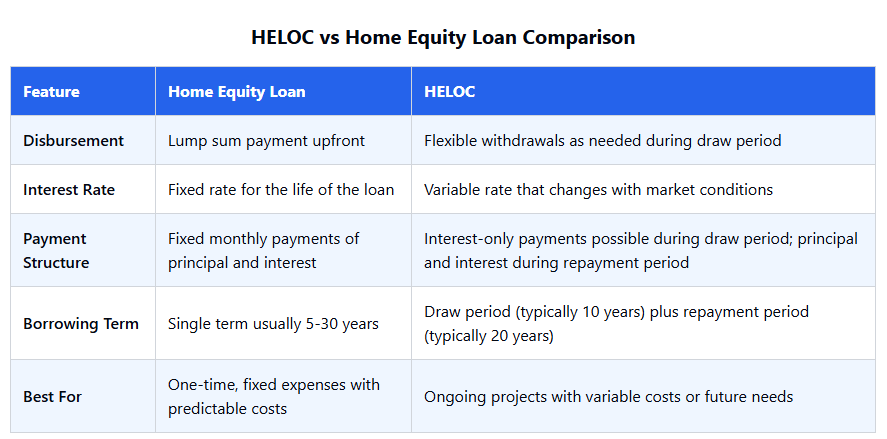

Home Equity Loan: The "Second Mortgage"

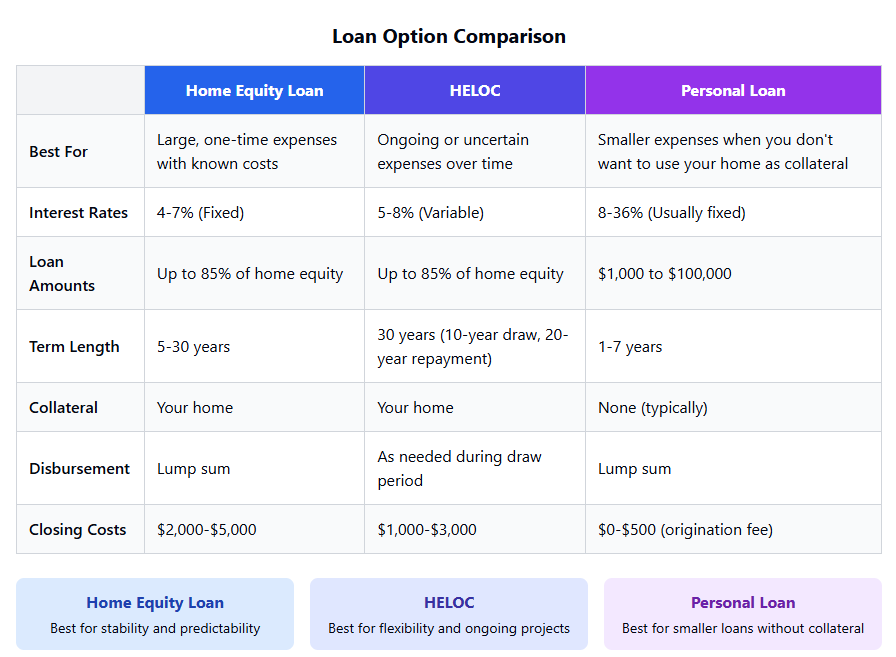

A home equity loan is often referred to as a second mortgage because it operates similarly to your primary mortgage. When you take out a home equity loan, you receive a lump sum of money upfront, which you then repay over a set period with fixed interest rates and consistent monthly payments.

How Home Equity Loans Work

When you apply for a home equity loan, lenders typically allow you to borrow up to 75%-85% of your available equity. Using our previous example with $150,000 in equity, you might be eligible to borrow between $112,500 and $127,500.

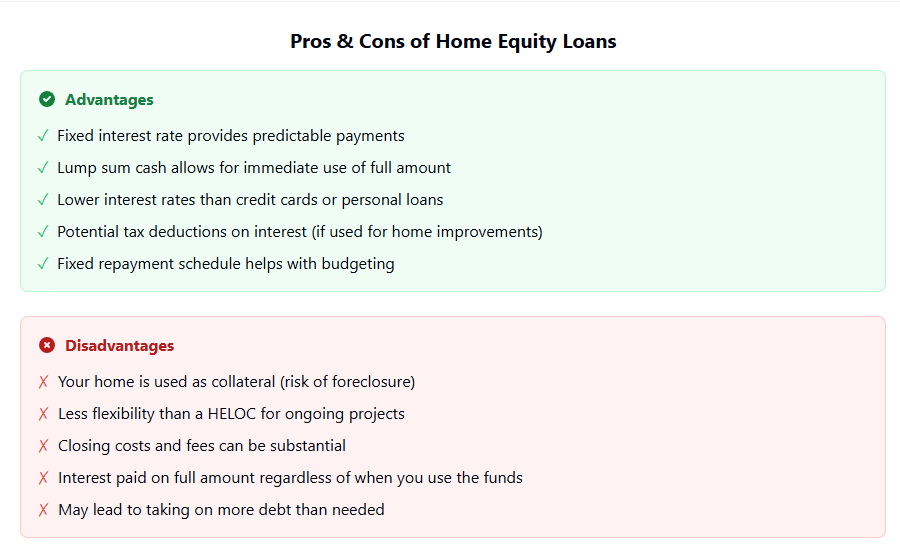

The loan term can range from 5 to 30 years, and since your home serves as collateral, interest rates are generally lower than unsecured loans like personal loans or credit cards. However, this also means your home is at risk if you fail to make payments.

Pros and Cons of Home Equity Loans

HELOC: The Flexible Credit Line

Unlike a home equity loan, a home equity line of credit (HELOC) functions more like a credit card. It provides you with a revolving line of credit that you can draw from as needed, up to your approved limit, during what's known as the "draw period."

How HELOCs Work

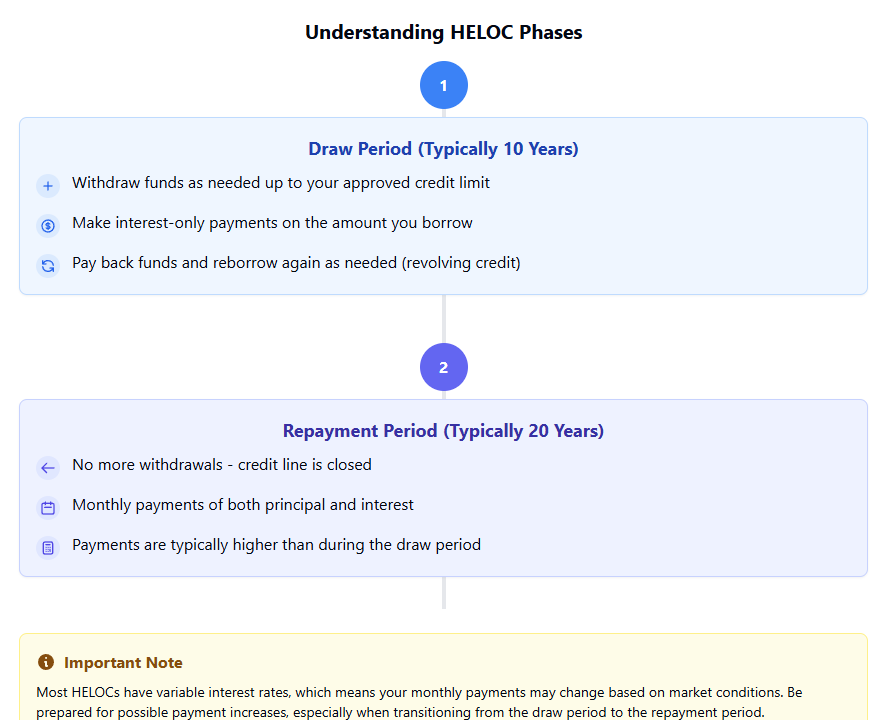

A HELOC is structured in two distinct phases:

- Draw Period: This initial phase typically lasts around 10 years. During this time, you can borrow from your credit line as needed, and you only need to make payments on the amount you've actually used. Many lenders offer interest-only payment options during this period, keeping your monthly payments relatively low.

- Repayment Period: Once the draw period ends, you enter the repayment phase, which usually lasts about 20 years. At this point, you can no longer withdraw funds, and your payments increase to cover both principal and interest.

Most HELOCs come with variable interest rates that can fluctuate monthly based on market conditions, which means your payment amounts may change over time.

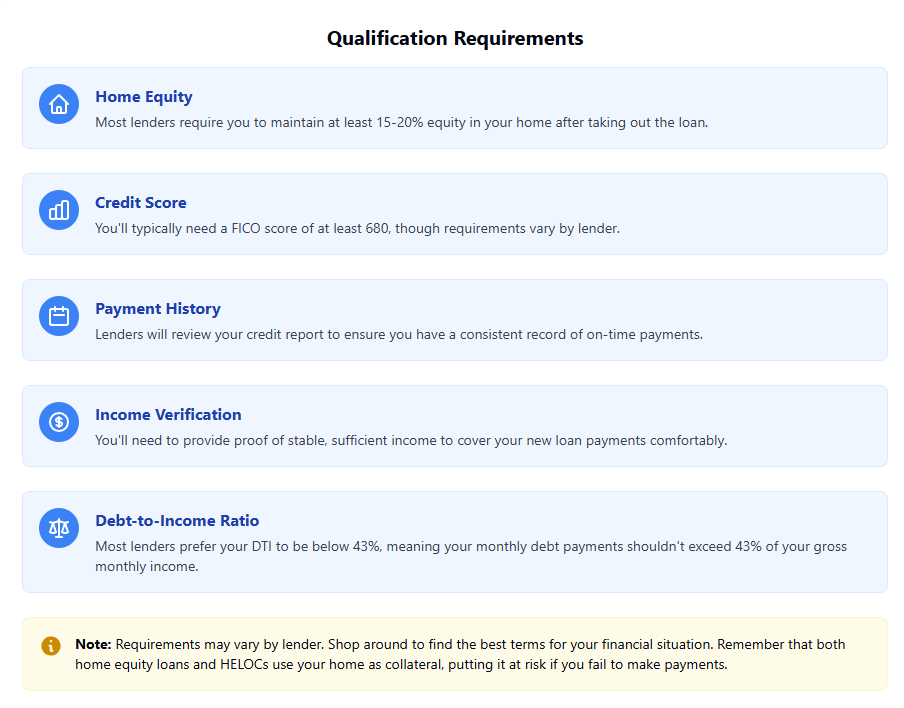

Qualifying for Home Equity Loans and HELOCs

Whether you're interested in a home equity loan or a HELOC, lenders will evaluate your application based on several key factors:

- Home Equity: Most lenders require you to maintain at least 15% to 20% equity in your home after taking out the loan.

- Credit Score: You'll typically need a FICO score of at least 680, though some lenders may accept lower scores if you have substantial equity or income.

- Payment History: Lenders will review your credit report to ensure you have a consistent record of on-time payments.

- Income Verification: You'll need to provide proof of stable, sufficient income to cover your new loan payments comfortably.

- Debt-to-Income Ratio (DTI): Most lenders prefer your DTI to be below 43%, meaning your monthly debt payments (including the new loan) shouldn't exceed 43% of your gross monthly income.

Making the Right Choice: Home Equity Loan or HELOC?

Your financial goals and preferences will largely determine which option is better for you:

Choose a Home Equity Loan If:

- You need a large, one-time sum for a specific purpose like a major home renovation or college tuition

- You prefer predictable, fixed monthly payments

- You want the security of knowing your interest rate won't change

- You're confident you won't need additional funds after the initial disbursement

Choose a HELOC If:

- You're working on a project with uncertain or staggered costs, like a DIY home renovation

- You want the flexibility to borrow only what you need, when you need it

- You're comfortable with variable interest rates that might change over time

- You prefer the option of making interest-only payments during the initial period

- You might need access to funds over an extended period

Personal Loans: An Alternative to Consider

If you're uncomfortable using your home as collateral or don't have sufficient equity, a personal loan might be a viable alternative. While personal loans typically have higher interest rates than home equity options (ranging from 8% to 36% depending on your credit profile), they don't put your home at risk.

Personal loans allow you to borrow anywhere from a few hundred dollars to $100,000, with repayment terms from one to seven years. Unlike home equity products, personal loans are typically unsecured, meaning you don't need to provide collateral.

Ready to access your home equity?

Get competitive rates and personalized service from experts who care about your financial future.

- ✓Low rates starting at 6.16 FHA%

- ✓Fast approvals — often in as little as 3 days

- ✓Dedicated loan officers who guide you through the process

No obligation. Free quote in minutes.

Categories

Recent Posts