The Hidden Cost of Waiting: Why Now Is the Time to Buy a Home

Everyone loves investing in things that appreciate over time—whether it’s rare coins, vintage cars, or fine art. But one of the most reliable wealth-building tools has always been homeownership. In today’s housing market, waiting for home prices or mortgage rates to drop might feel like the right move, but doing so could mean missing out on a major opportunity to build equity in a rising market.

The Current Housing Market at a Glance

- Home Prices: Home prices continue to climb in many markets, fueled by high demand and limited inventory. According to the Federal Housing Finance Agency (FHFA), home prices rose by 3.1% nationally in Q3 2024 compared to the previous year, and many experts predict steady growth into 2025.

- Mortgage Rates: Rates have stabilized but remain elevated, hovering around 6.74% for a 30-year fixed-rate mortgage, 6.12% for an FHA mortgage, as per Freddie Mac and at 6.15% for a VA loan.

The Power of Home Equity

Home equity is the portion of your home you own outright—essentially, your stake in a valuable asset. As home prices rise, so does your equity, creating a critical wealth-building mechanism for homeowners. Here’s why waiting could cost you:

-

Rising Prices Increase Equity: Home prices are expected to appreciate steadily, meaning buyers who act now can benefit from this growth. A $400,000 home appreciating at a modest 3% annually could gain $12,000 in value in just one year. Waiting to buy could mean forfeiting these gains.

-

Mortgage Paydown Adds to Equity: Each mortgage payment builds equity as you reduce the loan balance. Delaying homeownership means losing out on these contributions to your net worth.

-

Missed Opportunity to Leverage Low Inventory: The limited supply of homes has created a competitive market. When rates and prices fall, buyer demand typically surges, leading to bidding wars that could drive prices higher, eroding any perceived savings.

Historical Trends: When Prices Drop, Competition Rises

A lower interest rate environment often brings more buyers into the market, increasing demand for limited housing stock. This typically sparks bidding wars, driving prices higher. For example:

- During the 2020-2021 pandemic housing boom, historically low interest rates created intense competition, pushing prices up by over 18% year-over-year in some markets.

Delaying your purchase could mean entering a more competitive environment down the road, where the same homes may cost more due to increased demand.

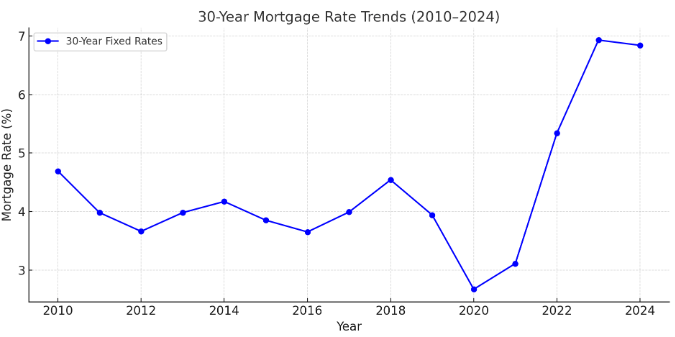

Mortgage rates fell dramatically during the COVID-19 pandemic, reaching historic lows near 2.7% in early 2021. Rates began climbing in 2022 due to inflationary pressures and Federal Reserve rate hikes, peaking at around 7.1% in late 2022. As of November 2024, the average 30-year fixed mortgage rate is 6.84%, reflecting a modest decline from its peak.

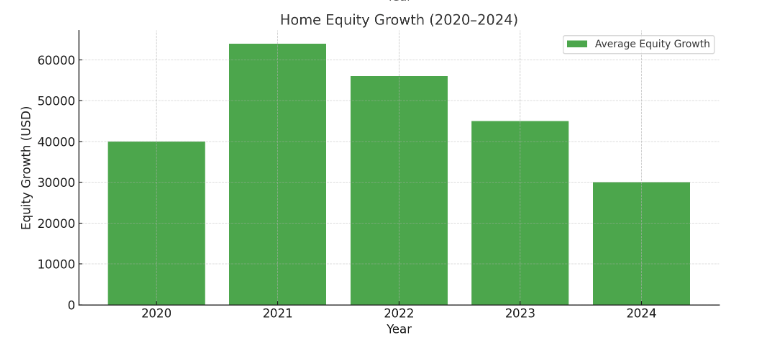

Home Equity Growth (2020–2024):

Between 2020 and 2023, U.S. homeowners gained significant equity due to rising home values. In 2021 alone, the average equity gain per homeowner was approximately $64,000. This trend continued, albeit slower, into 2023 as price appreciation cooled but remained positive.

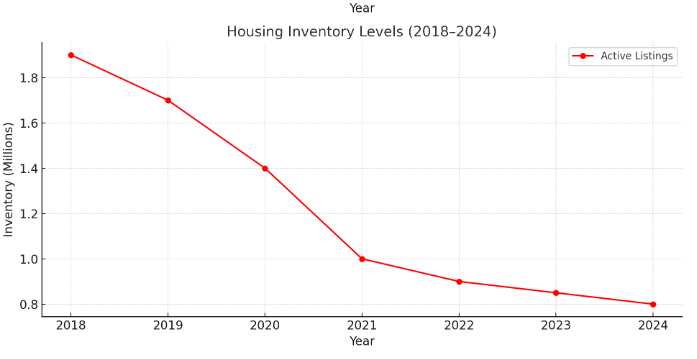

Housing inventory has been declining steadily since 2018. The pandemic exacerbated this trend, with a 40% drop in available homes for sale between 2019 and 2021. Inventory remains constrained as of 2024, hovering near record lows.

Categories

Recent Posts